As Canada’s financial capital, Toronto is considered an international centre for business and finance. It is home to the Big Five, a name for the five of Canada’s largest financial institutions. Moreover, the Toronto Stock Exchange is the world’s seventh-largest stock exchange in terms of market capitalization and has a high concentration of banks and brokerage firms that further cements its economic trademark. Its sectors in media, telecommunication, film production and information technology are also worth noting.

In terms of population, Toronto is the largest city in Canada and fourth largest in North America. The 2016 census reported a total population of 2,731,571, a 4.5% increase against 2011, with a large portion (69.8%) belonging to the 15 to 64 age range. Data shows that there has been a shift in age distribution; more people are over 65 than there are under the age of 15. The average and median ages are slightly lower than Ontario’s at 40.6 and 39.3.

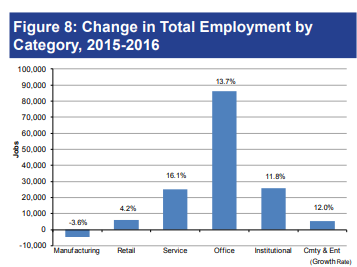

The 2016 unemployment rate in Toronto is 8.2%. The survey totalled 1,461,020, jobs which showed an increase of 2.7% against 2015 data, with the majority of employed individuals in the office sector.

Because Toronto’s economy is continuously growing, a significant amount of jobs are expected to be generated as the city sees more and more businesses and investors.

Toronto started 2017 strong, with roughly 2.7% in economic growth coming from the finance, insurance, and real estate industries. It is a growth leader among the 13 CMAs according to the Conference Board of Canada’s Metropolitan Outlook: Spring 2017. Toronto also expects to see its manufacturing industry grow.

The increase in sales and prices of the Toronto housing market shows healthy growth. With roughly 500 communities in the region, Toronto’s supply could be an issue in the future. According to the Toronto Real Estate Board, it is vital to work with realtors with a familiarity with the local market conditions before investing.

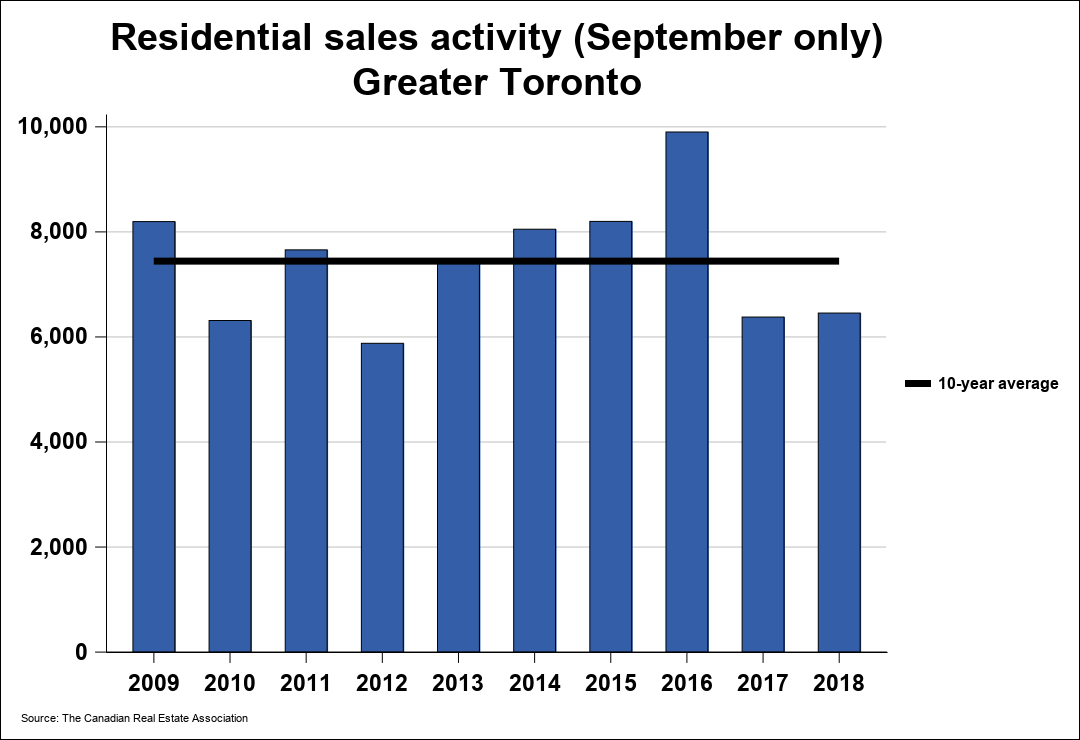

There were 6,839 homes sold in August 2018, reflecting an 8.5% increase versus August last year. The population of the region continues to grow, which may explain the need for more housing options. Supply, rather than demand, will be the future concern.

Toronto’s mortgage qualifications are tighter in 2018. Borrowing costs are also higher this year versus the past years. Despite this, many buyers and investors are optimistic that homeownership is an excellent long-term investment decision.

The average sales price of Toronto housing units grew by 4.7% from $730, 969 in August 2017 to $765,270 in August 2018. Year over year, both sales and pricing continue to rise. Buyers and investors are both confident about the outcome of their Toronto investments.

The Toronto Real Estate Board reports show that annual price growth is getting stronger for higher density home types, which include condominium apartments, townhouses and semi-detached units. In other neighbourhoods, these housing types are more affordable.

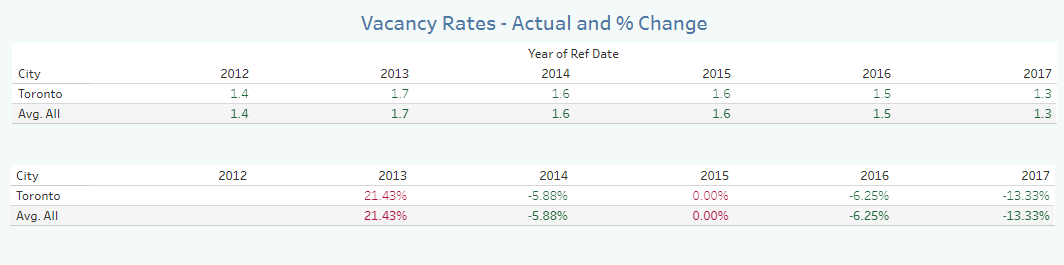

The city of Toronto has less than two months of supply available for the increasing demand for housing in the market, according to the Toronto Real Estate Board. Sales have been off the record highs since 2016 and 2017. Currently, various areas continue to experience a lack of inventory. Vacancy rates continue to drop year over year since 2013. Back in 2017, the year closed with 1.3 vacancies.

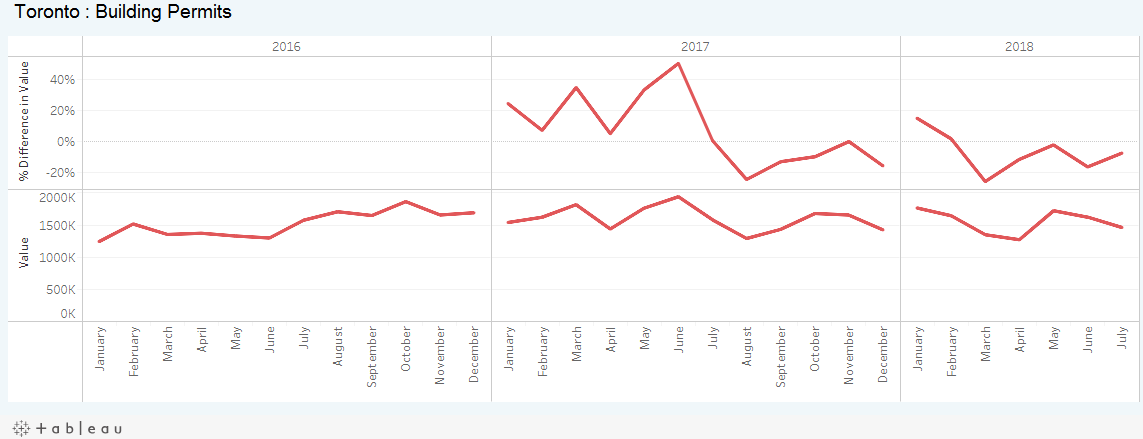

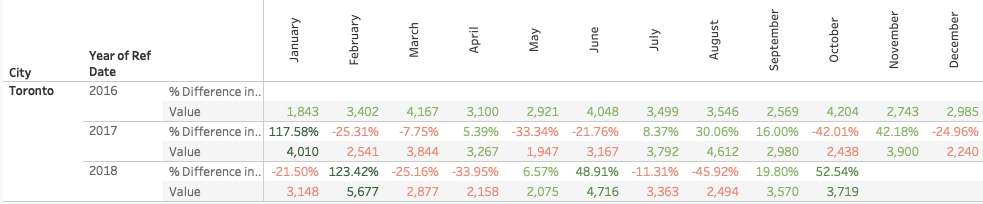

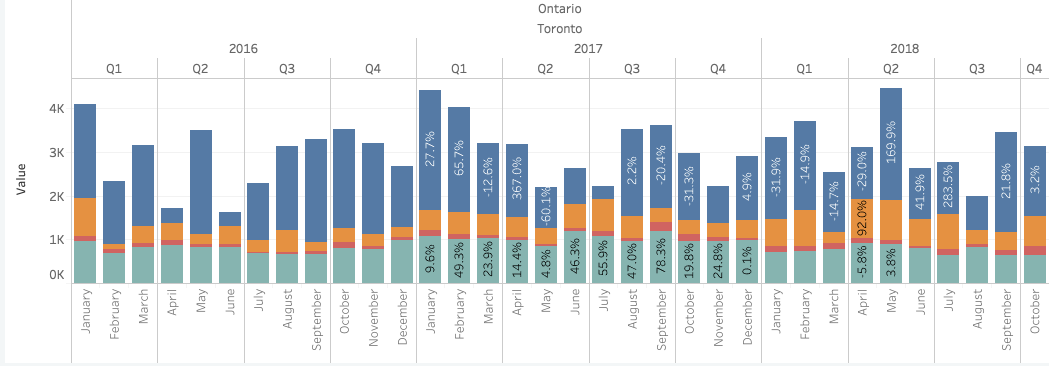

The latest building permits data as of July 2018 showed that the total value for permits was $10,782,392 for Toronto. This seasonally adjusted figure is still short by 43.50% in comparison with last year’s permit issuance.

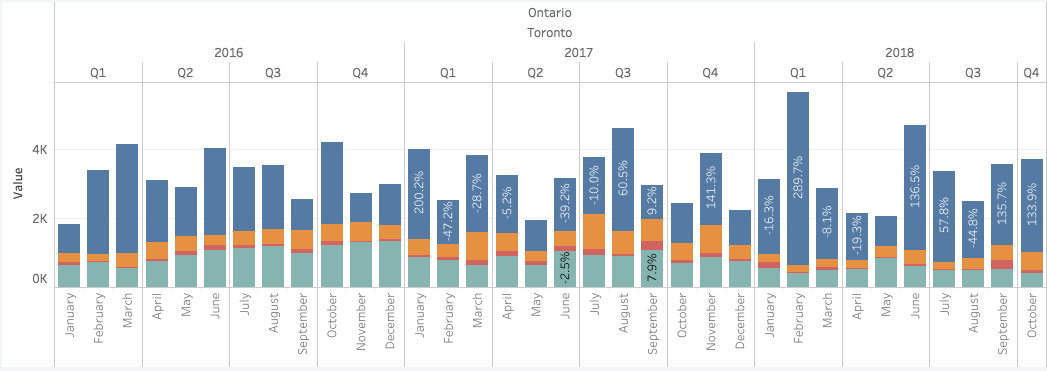

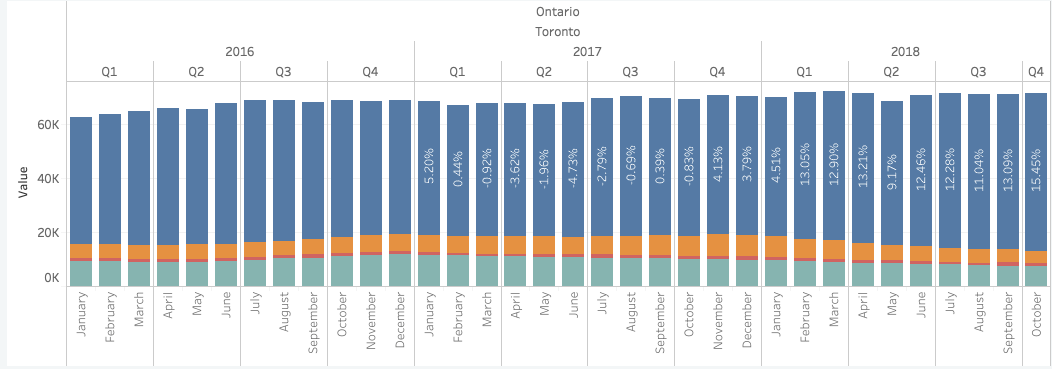

There were a total of 3,719 housing starts from the latest October figures representing a 52% increase year-over-year. Apartment units led the way with a share of 72% of the total housing starts representing a 133% increase from October of 2017. While there was a slight slump in August where housing starts saw the steepest decline year over year for 2018 at 45%, the figures rebounded sharply in September posting a 52% year over year growth.

Apartment units have made up the majority share of this contribution, making up for the continued loss in the single-detached units sector where starts have been seeing a constant 40%+ decline each month compared to the previous year for the same month.

With supply becoming a significant concern in the region, the number of housing under construction units have maintained a definite trend to cope with the growing demand of the market. Month after month, housing under construction for 2018 is trending higher compared to last year.

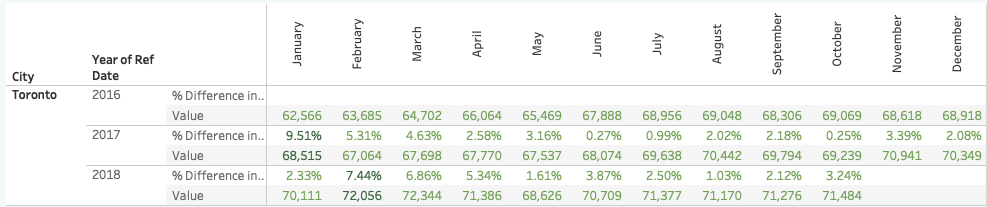

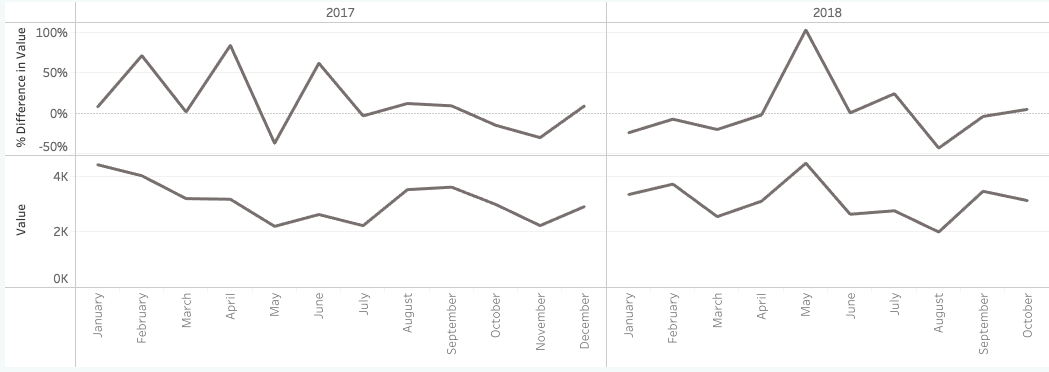

As of October 2018, housing under construction totalled 710,539 units and is on pace to be slightly higher compared to 2017. While the first half of 2017 saw double-digit year over year growth in the single-family detached sector, the positive course began to change in September of 2017 and has continued to decline ever since. Row-units have been on a decline as well since April of 2018 and falling to a 6.6% representation of total homes under construction. It has been apartment sector that has kept the total pace of units trending upwards. From October 2017 to October of 2018, the market share of apartments has gone up by almost 10% representing nearly 82% of all housing under construction compared to 73% in October of 2017 (15% increase YOY).

May of 2018 saw the largest year-over-year increase with 103% more homes completed compared to May of 2017. Apartment units were responsible for the majority of this spike with a 170% increase year over year. This brought on just over 2,500 new apartment units on the market in May. While 2017 witnessed positive year over year figures for the single-detached sector for each month, 2018 has shown an opposite trend posting negative figures typically in the double-digit range for nearly every month.

The amount of new housing inventory coming on the market throughout 2018 has seen swings in both directions. However, the amount of housing completions does seem to have been on a relative decline from August until November.

While 2017 saw a strong rate of housing inventory absorbed, the trend has entered negative figures since May of 2018 and hitting a year-over-year low in July with a 40% reduced absorption rate compared to the same month a year before.

Real estate properties, one of the core investment products in Toronto, continue to gain strong sales performance with pricing that has aggressively increased. The growing population of the region may result in future supply concerns in the housing market.

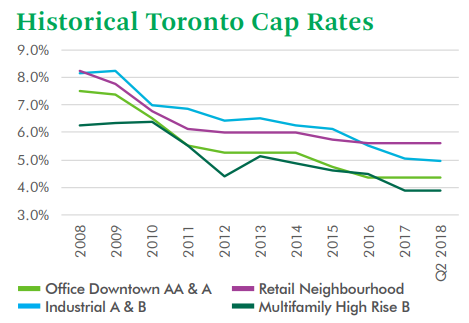

Toronto’s investment returns have steadily created an abundance of liquid investors in the region. The second quarter Cap Rates include 4% to 5% for downtown offices, 5.5% to 7.25% for suburban offices, 3% to 4.25% for high rise multifamily properties and 3% to 4.5% for low rise multifamily developments.