The city of Niagara Falls is located in the regional municipality of Niagara, southeastern Ontario Canada. It is at the port of the Niagara River just opposite the Niagara Falls, New York. Because of its proximity to the United States, the city has several bridges connecting both countries, including the Rainbow, Whirlpool, and Queenston-Lewiston bridges.

The city has multiple commercial and natural attractions such as Queen Victoria Park, Lundy’s Lane museum, Maid of the Mist Marineland, Skylon Tower and Pavilion, Butterfly Conservatory, Canada One Factory Outlets, and the Canadian Falls, to name a few.

There has not been any significant increase in the population of Niagara Falls between 1996 and 2016. In fact, the latest 2016 census report showed only a 6.1% increase from 2011. This brings Niagara’s total population to about 88,071, with 64.7% belonging to the 15 to 64 age group and putting the average and median age at 43 and 45, respectively.

Income levels in private households remain relatively low. As of 2015, the median income was at $29,275 while average total income came to $38,360.

The ManpowerGroup Employment Outlook Survey for the fourth quarter of 2019 collected information from 1,930 employers from Canada.

The hiring climate for Niagara Falls is cautious. Of the respondents from this city, 76% expected workforce levels to remain the same, 7% were planning to hire, but 17% were anticipating human resource cuts.

On the other hand, St. Catharines describes their hiring sentiment as cautiously optimistic. 10% were planning to hire, another 10% were anticipating cutbacks, and 80% were predicting their staffing levels to remain constant.

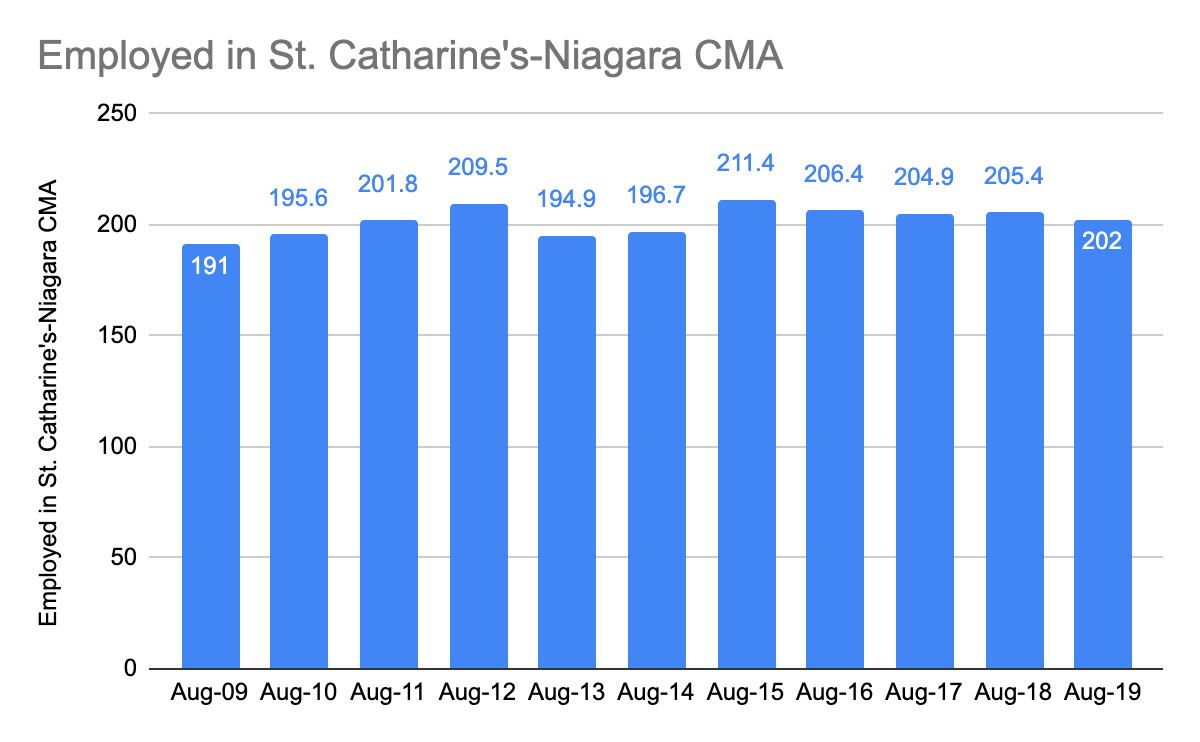

These sentiments are somewhat consistent with the overall employment data for the St. Catharines-Niagara region, which saw a slight drop of 1.66% versus the previous year. The unemployment rate of the census metropolitan region is at 5.8%, just slightly higher than the Ontario rate of 5.6%.

Source: Labour Force Survey

St. Catharines-Niagara’s economy continues the slow and steady growth observed in the region in the past few years. The increase is expected to come from commercial construction, exports, and retail. Real GDP is forecast to expand by 1.43% in 2018 and 1.38% in 2019, which is a continuation of the moderate growth achieved in the region in previous years.

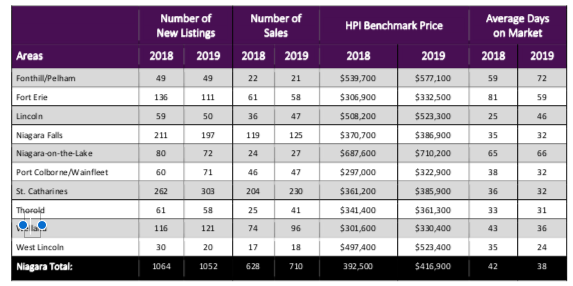

Niagara home residential sales continue to be stable, as pointed out by Niagara Association of Realtors (NAR) President Deanna Gunter. “This sets a nice foundation for buyers and sellers as we head into the fall market.”

The NAR reported a total of 710 property sales for August 2019, 13% higher than the same month of the previous year, and only 0.7% lower than the last month. There has also been an improvement in the average days needed to sell a house, which is currently at 38 days, versus the 42 required in the previous year. However, this month’s rate is slightly longer than the last month, which only needed an average of 35 days to complete a sale.

The HPI Benchmark Price for the region is currently at $416,900, which is 6.2% higher than the previous year’s price of $392,500 and virtually unchanged from the last month’s $416,700. There were 1,052 new listings in August 2019, only 1.1% lower than the previous year’s 1,064.

Vacancy rates for rental units have been dropping from 2015 to 2017. However, the vacancy rate in 2018 increased by 78.57%. Nevertheless, it remains to be low in absolute terms.

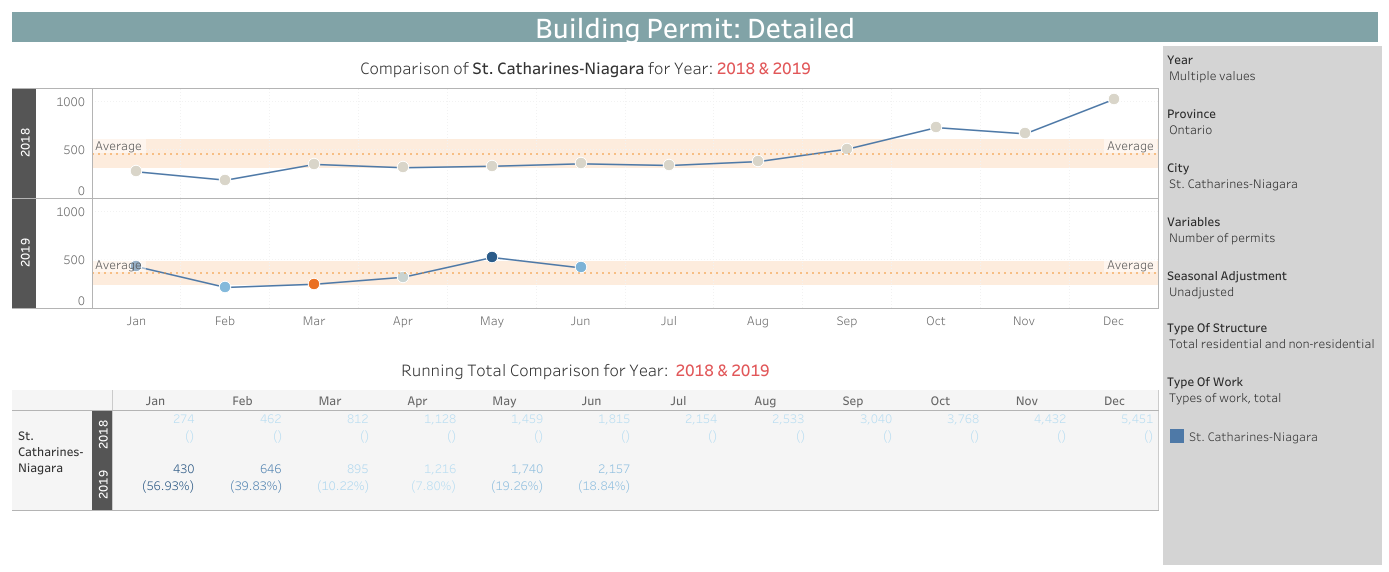

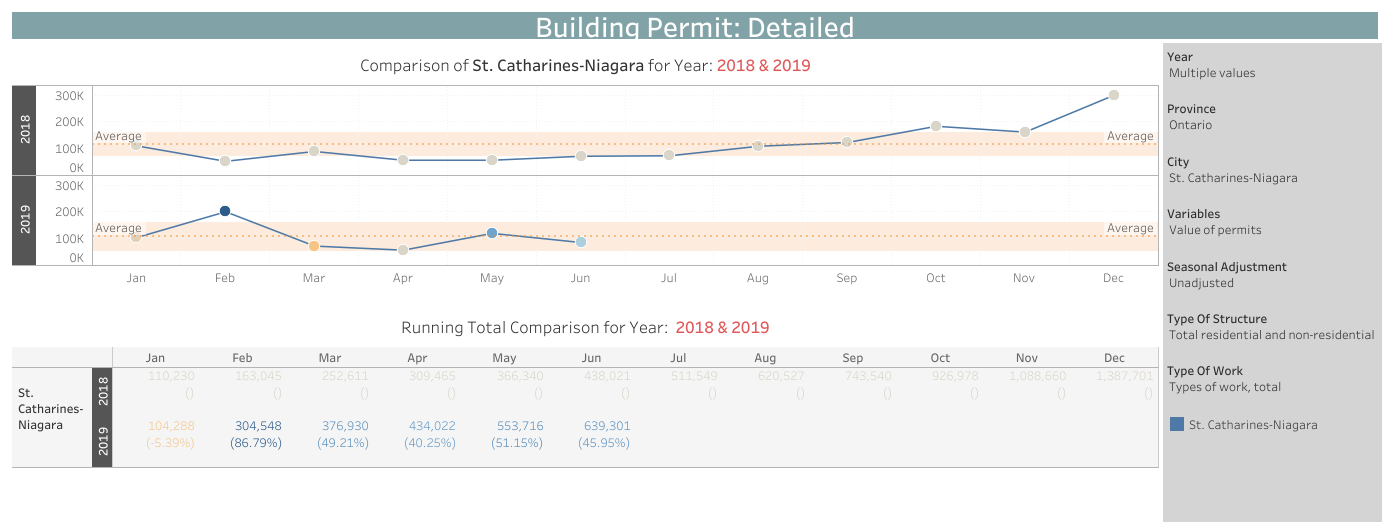

A total of 2,157 building permits were issued in the St. Catharines-Niagara CMA for the 1st half of 2019, which peaked at 524 in May and averaged 359 permits for this period. The 1st semester total is also 18.84% higher than the same period of the previous year, which was at 1,815 permits issued. However, issuance of building permits in the 2nd half of 2018 continuously accelerated, which peaked in December with 1,019 released and brought 2018’s total to 5,451. Permits issued in January 2019 dropped by 57.8% versus the previous month. If we annualize the current average, the permits issued for the full year of 2019 will be 21.0% lower than 2018.

The cost of the building permits issued in the metropolitan region for the 1st half of 2019 amounted to $639.3 million, 46.0% higher than the same period of the previous year, which had a value of $438.0 million. If we annualize the 2019 average, the full year for 2019 will be 20% lower than the entire year of 2018.

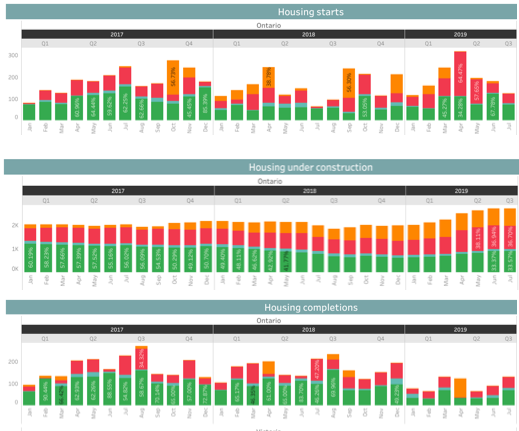

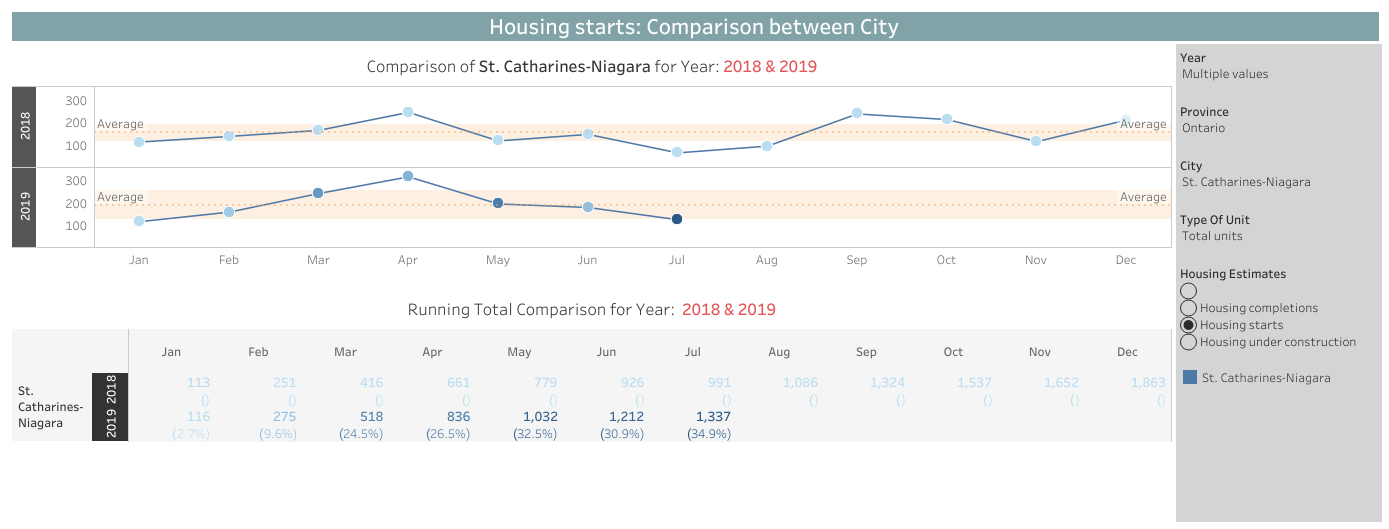

The southern Ontario metropolitan region registered 1,337 housing starts as of July 2019, 34.9% higher than the previous year. The year started slowly, as the 116 housing starts in January was a 45% drop versus last month. However, developers picked up the pace as there was a continuous increase which peaked at 318 starts in April. The trend reversed in the following months, as housing starts slowed down, with only 125 housing starts in July. Nevertheless, 2019 is on track to match or surpass the 2018 performance given that there are still five months remaining in the year, the current year’s housing starts already reaching 71.8% of the previous year’s total.

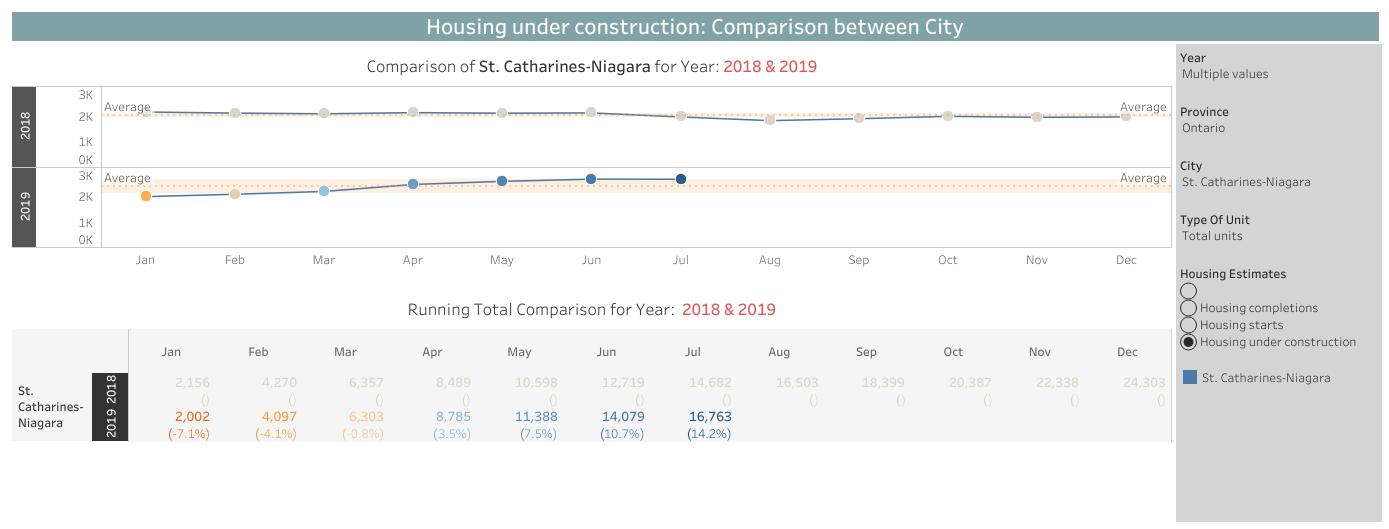

The inventory of housing under construction in the St. Catharines-Niagara region has observed a slight and gradual rise in 2019 after a very stable year in 2018. Last year averaged a total of 2,094 units under construction, with values falling between 1,821 and 2,156. This year saw this number peak at 2,691 units in June, which brought the 2019 average to 2,127 units, roughly 1.6% higher than the previous year.

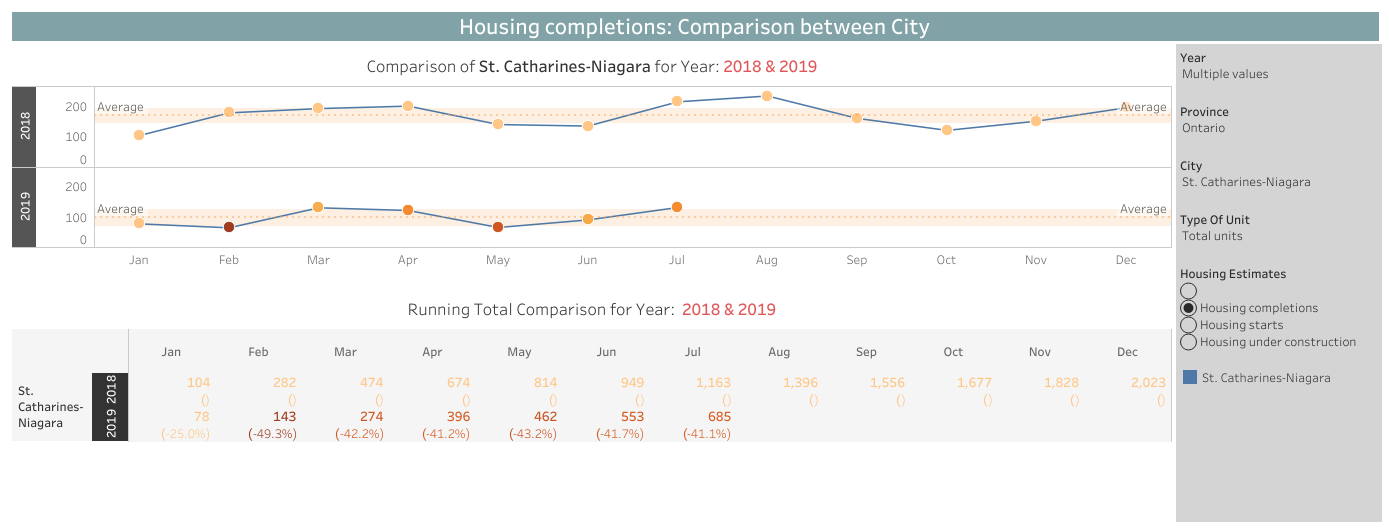

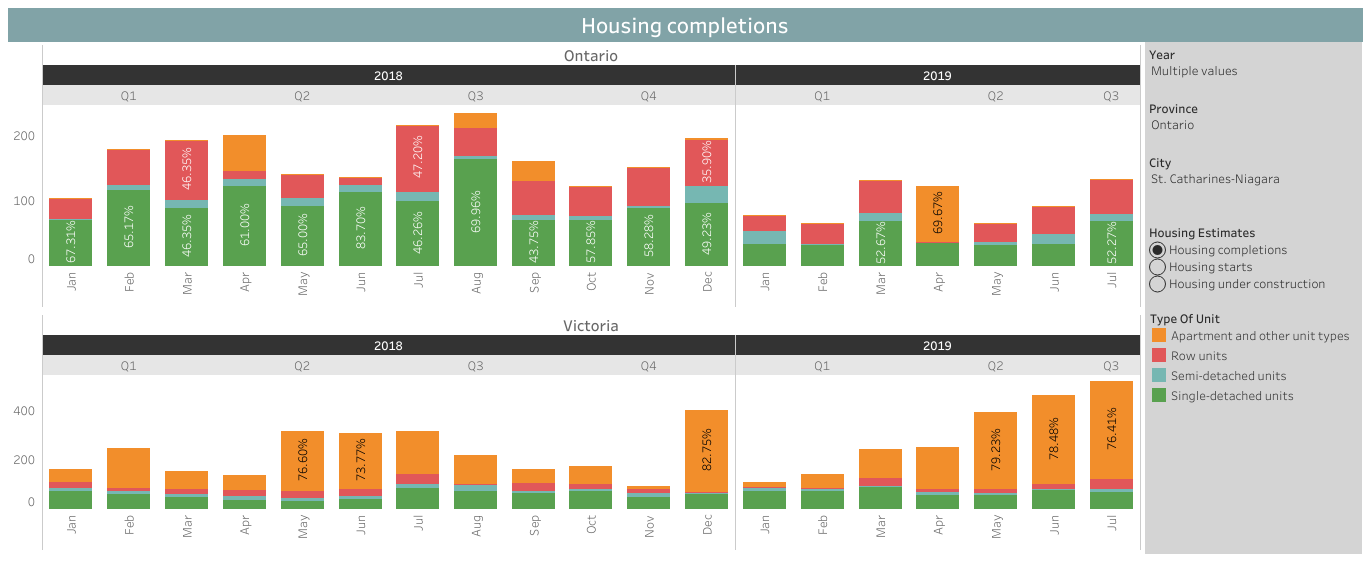

There were 685 housing units completed as of July 2019, a 41.1% drop versus the same period of the previous year. The seven-month figure is also 33.8% of the full-year total of 2018. The housing completions ranged from 65 to 132, with an average of 97 completions per month, in contrast with the previous year’s range of 104 to 213 and 168 average completions.

Of the 685 units completed, 45% or 305 units were single-detached homes, while 34% or 232 were row houses. Apartments contributed 85 units or 12% of the completions, while semi-detached houses added 62 units or 9% of the total. Single-detached homes and row house completions were significantly lower than the previous year, declining by 56% and 31% respectively, while semi-detached completed 9% fewer homes. On the other hand, the number of apartments built grew by 47%.

585 of the 685 units completed as of July 2019 were absorbed. However, this figure is 45.1% lower than that of the same period last year. The volume of single-detached homes declined by 55.7%, while row houses were 27.2% fewer than the past year. Absorption for semi-detached homes dropped by 18.6%

Construction activity seems to be quickening as there were 1,337 housing starts recorded in 2019, an increase of 34.9% versus the previous year, with 685 housing units completed. The inventory of housing units under construction increased by 652 during this period. The growing number of housing starts coupled with fewer completions increased the stock of housing under construction by about 30% in 2019. There is a need to monitor this trend, notably as absorption among all housing types have declined versus the previous year. Completions are expected to increase given the growth in starts, and if take-up does not improve, then there will be an increased number of units completed and unabsorbed. Homebuilders may be conscious of this trend, as the issuance of building permits has already started to slow down. Nevertheless, we need to monitor row house statistics more closely; this type of housing unit had more starts versus previous years and an absorption rate of 63.8% as of August 2019. On the other hand, 100% of single-detached and semi-detached housing listed for sale were absorbed.