When a potential home buyer approaches you to help them navigate the mortgage process and ultimately finance their home, one of the first questions that’s asked is about their credit.

To qualify for the best mortgage rates from traditional lenders, borrowers generally need a credit score of 680 or above. If your client has a lower score, that doesn’t mean that financing isn’t available to them, but they may have to expand their search for a lender to finance their purchase.

Private lenders like CMI are able to provide more flexible financing because they are able to look at a borrower’s circumstances more broadly compared to traditional banks and lenders. Private mortgages can be used as a debt consolidation tool, which can help improve a client’s credit scores to a level where they may eventually qualify for a conventional mortgage at a lower rate.

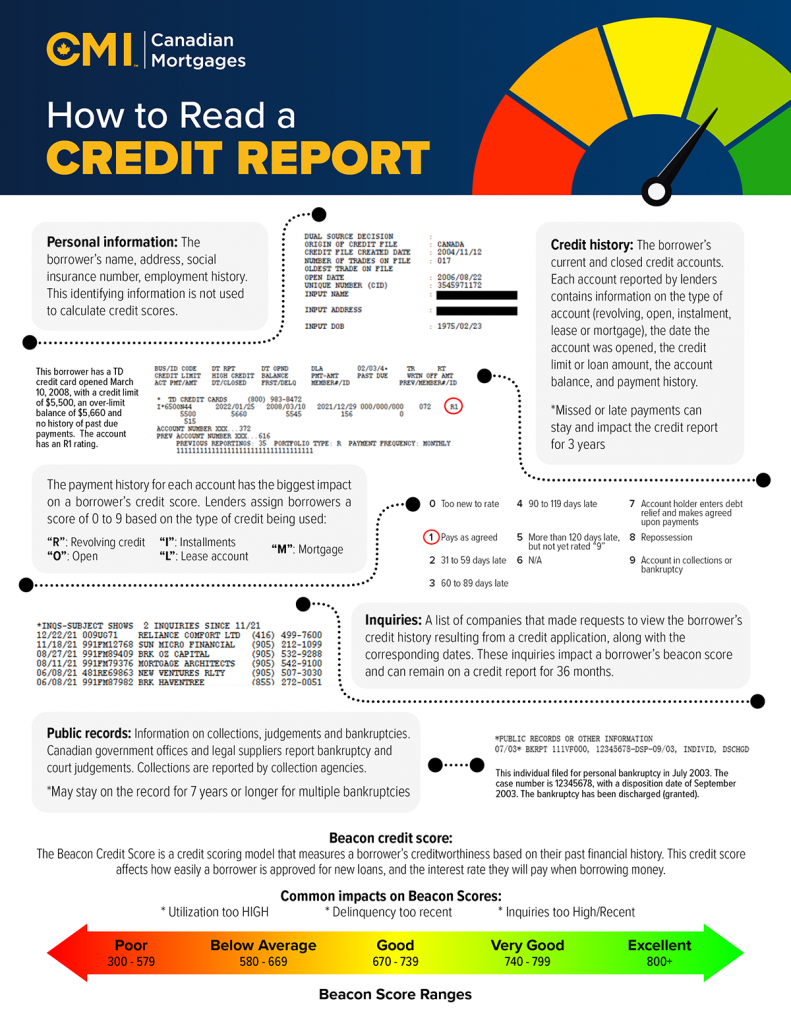

Borrowers understand that their credit score is important, but it’s helpful to educate clients on why it’s important, and how credit scores are calculated, including the various factors that impact the score. For those with damaged credit, understanding the factors and the types of accounts that affect their credit score can help them improve their credit over time.

Credit scores typically range between 300 and 850 points and provide an indication of a borrower’s capacity r to repay their loans. There are two main credit bureaus in Canada – Equifax and TransUnion – that collect, store, and share information about how you use credit.

There are five main factors used to calculate credit scores:

Payment History

The most important factor in a credit score is whether a borrower has a good track record of repaying the money loaned to them. Payment history comprises up to 35% of a credit score. Remind clients that multiple late or missed payments, overdue accounts, bankruptcies and any written off debts will all lower their credit score. Paying back debt quickly can help repair their credit.

Credit Utilization

Credit utilization ratio looks at the percentage of debt used out of all credit limits available to the borrower. If your client has multiple credit cards, revolving lines of credit or other accounts that are maxed out consistently, it can lower their credit score. Help clients examine the type of accounts they hold and stress the importance of managing each of them responsibly.

Credit History

The longer someone has an account open, the better for their credit score. Credit history is a window into how much experience a borrower has managing debt and their ability to pay it off. Work with clients to review active and inactive accounts. Suggest leaving credit card accounts open, even if they don’t use them much, as the age of the account might help boost their score.

New Credit

New credit is another key input to a person’s credit score. Check with clients to see how recently and how often they’ve applied for new credit, as well as how many new accounts have actually been opened. When you apply for new credit, borrowers are subject to a “hard inquiry” so that the lender can check their credit information. If there have been many of these hard credit checks in a short period of time, it could impact their credit score negatively.

Types of Credit

Having more than one type of credit account (while managing them responsibly) can improve your client’s credit score, such as credit cards, an auto loan, mortgages, and lines of credit. This makes up a smaller portion of a borrower’s score, but balancing different types of credit can be a way to raise your client’s score.

Partner with CMI today and see why we’re preferred by brokers across Canada. With access to more than $1 billion in capital, we lend everywhere from cities to towns and everything in between.